BYD’s Wang said in the 2025 shareholders meeting.

Interesting.

But the target itself isn’t the story.

The engineering stack behind it is.

Most people see an EV company.

I see a company systematically removing dependencies across the entire automotive value chain.

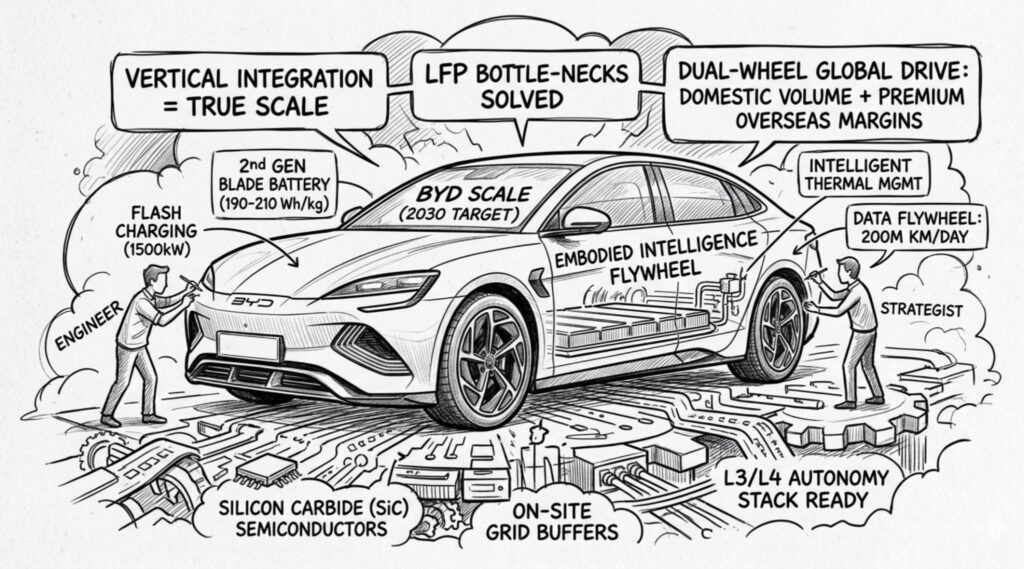

Three things stood out from Wang Chuanfu’s shareholder meeting:

1. They’re rebuilding the hardware baseline.

BYD isn’t simply increasing production.

They’re pairing next-generation Blade Batteries with ultra-fast FLASH charging technology to attack two of LFP’s biggest historical weaknesses: charging speed and cold-weather performance.

2. They’ve built a massive data flywheel.

More than 3.1 million intelligent-driving vehicles are already on the road, generating around 200 million kilometers of real-world driving data every day.

That’s not just a fleet. It’s a neural network training engine waiting for L3/L4 regulations to catch up.

3. They’re using global markets to protect margins.

Rather than fighting endless price wars at home,

BYD is pushing premium brands like Denza and Yangwang overseas, leveraging its manufacturing cost advantage to absorb the cost of advanced software and hardware.

The bigger lesson?

The next automotive leaders won’t win because they assemble cars more efficiently.

They’ll win because they control the stack:

→ Battery chemistry.

→ Power semiconductors.

→ Vehicle software.

→ AI algorithms.

→ Manufacturing.

→ Energy infrastructure.

→ The data generated by millions of connected vehicles.

In the SDV era, scale is no longer measured only in units sold.

It’s measured by how much of the ecosystem you own.

The question for legacy OEMs isn’t whether they can build a competitive EV.

It’s whether they can build a competitive vertical integration model before software, AI, and extreme fast charging redefine the economics of the industry.

✍️ How do you see traditional global platforms adapting to this new playbook?